A generation ago, the idea of a couple in their late fifties filing for divorce in an Indian family court was almost unimaginable. Marriages were endured, sometimes with grace, often without. The children were the reason. The community was the reason. The pension was the reason. People stayed.

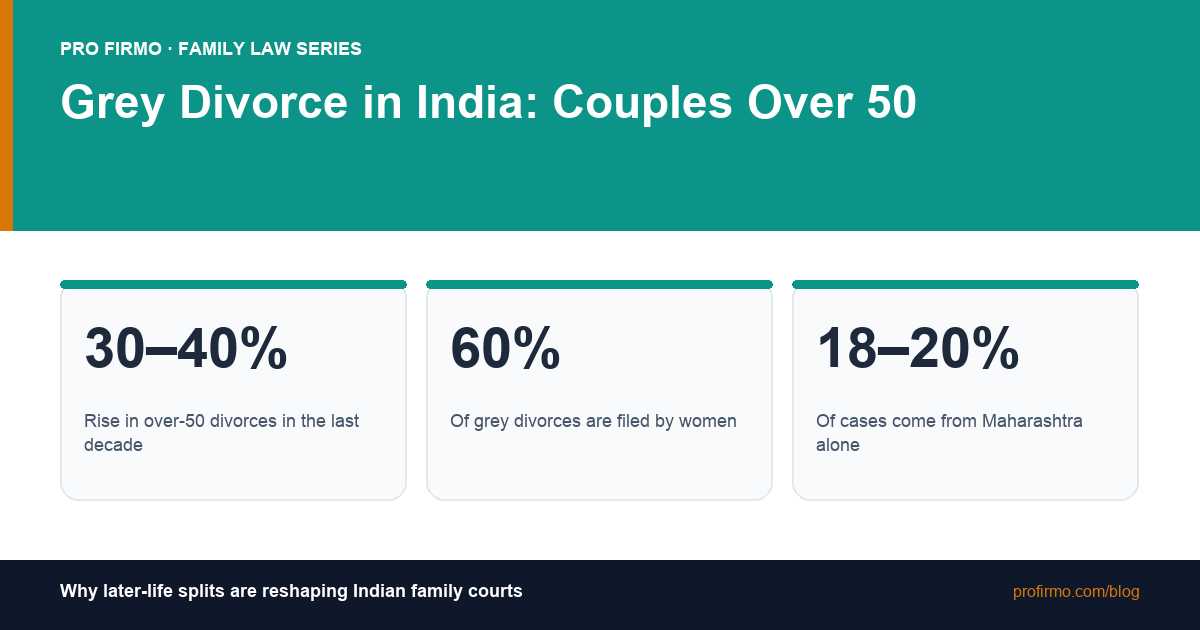

That arithmetic is changing fast. Senior family-court lawyers in Mumbai, Delhi, Bengaluru, and Hyderabad now estimate a 30 to 40 percent rise in divorces among couples over 50 in the last decade. Mumbai's family courts reported a roughly 10 percent year-on-year jump in over-50 filings between 2020 and 2024. Maharashtra alone now accounts for nearly 18 to 20 percent of all grey divorces in India, followed by Delhi, Karnataka, and Tamil Nadu.

Perhaps the most telling statistic: over 60 percent of these later-life divorces are filed by women.

This isn't a Western trend that has accidentally arrived in India. It is a distinctly Indian shift, driven by the way the country itself has changed in one generation. Let's look at what's actually behind it — and at what changes when you're navigating a divorce at 55 or 65 rather than 35.

What's driving grey divorce in India

1. Women's economic independence. The single biggest change. Women in their fifties today were among the first cohort to enter the urban Indian workforce in serious numbers in the 1990s. Many of them have their own PF accounts, NPS holdings, equity portfolios, and — crucially — their own bank balances. The financial calculation that historically kept Indian women in unhappy marriages no longer holds.

2. The empty nest. Indian parents are masters of "staying together for the children." For two or three decades, the children's school, then college, then settlement, then marriage become the organising principle of the household. When the last child leaves home — often to study or work abroad — both spouses find themselves alone with each other in a way they haven't been since their twenties. For many, what was workable at 35 with children in the house becomes intolerable at 55 without them.

3. Longer, healthier lives. A 55-year-old today can reasonably expect another 25 to 30 active years. The "grin and bear it till retirement" approach made some sense when retirement was a brief interlude before death. It makes less sense when retirement is itself a third of adult life.

4. Reduced social stigma. Especially in metros, divorce is no longer the calamity it was. Children of divorced parents are now common in any urban friend circle. Older couples watch their nieces and nephews divorce and remarry, and the unthinkable becomes thinkable.

5. Adult children pushing for it. A consistent observation from family-court counsellors: many grey divorces are quietly championed by the adult children, especially daughters who have watched their mothers absorb decades of one-sided marriage and are no longer willing to pretend it's fine.

How a grey divorce is legally different

The statute is the same — for Hindus, the Hindu Marriage Act, 1955; for Muslims, the Dissolution of Muslim Marriages Act; for Parsis and Christians, their respective acts; and the Special Marriage Act for inter-faith and civil-registered marriages. But four issues hit harder when the couple is older:

Alimony and post-retirement maintenance

The Supreme Court has been explicit (most recently in Kiran Jyot Maini v. Anish Pramod Patel, 2024) that permanent alimony should ensure the dependent spouse continues to enjoy a "decent standard of living" comparable to what they had during the marriage. For a wife who's been at home for 30 years and is now 55, that means a meaningful monthly maintenance for the rest of her life, or a substantial lump-sum settlement. Courts now use an eight-factor test (social and financial status, reasonable needs, qualifications and employment status, independent income or assets, marital standard of living, employment sacrifices, dependent-care responsibilities, litigation costs) — not a fixed percentage.

Pension and PF division

Provident Fund accumulations, pension entitlements, gratuity, and post-retirement medical cover are all on the table in a grey divorce. Government employees' pensions are subject to specific rules under the relevant pension schemes. Private-sector NPS and EPF accounts are part of the marital asset pool. Courts will look at the contribution history and the years of marriage to decide a fair split, often by carving a portion of monthly pension to the dependent spouse, or by adjusting other assets to equalise.

The matrimonial home

For couples in their late fifties, the home is usually paid for, lived in for 25 years, and full of memories. Selling it is emotionally hard even when it's financially clean. Two patterns are common:

- One spouse retains the home and pays the other their share of the equity from other assets or a long-tenor settlement.

- Co-ownership continues, with one spouse occupying and the other compensated through monthly maintenance plus a percentage of any future sale.

Either way, the right of residence under the DV Act for a dependent wife is well-settled — she cannot be evicted from the matrimonial home without alternative accommodation.

Wills, nominations, insurance

The forgotten paperwork of grey divorce. After the decree, every nomination needs to be reviewed: PF, NPS, life insurance, bank accounts, demat accounts, property. Without updating, the ex-spouse may still be the legal beneficiary of a life-insurance policy or the nominee on an EPF account — and a court fight after death is the worst kind of fight.

What good financial planning looks like

The single best piece of advice from senior matrimonial lawyers is: start the financial workout before you start the legal one. Couples who walk into a lawyer's office with a clear two-page summary of joint assets, individual assets, liabilities, and income from both sides save themselves months of fact-finding.

For the dependent spouse:

- Get a CA to prepare your projected income statement post-divorce — what you will receive, what you will spend.

- Get medical insurance in your own name before the decree; floater policies often disappear post-divorce.

- Build a settlement that includes a lump sum (for your immediate corpus) and monthly maintenance (for your day-to-day) rather than betting everything on one or the other.

For the higher-earning spouse:

- Don't try to "win" the settlement. Courts will not let you walk away cheap from a 30-year marriage. The faster you accept that, the cheaper and faster the divorce becomes.

- Plan tax. Lump-sum settlements are non-taxable capital receipts; recurring maintenance is taxable in the recipient's hands. The structure has real tax consequences for both sides.

Life after the decree

Grey divorce is hard. Loneliness is real, especially in the first 12 to 18 months, and especially for spouses whose social world was tied to the marriage. Most metros now have informal support groups and counsellors who specialise in later-life separation. Many divorcees in their late fifties report, two or three years on, that the loneliness was a price worth paying for honesty.

Indian society is still catching up to that arithmetic. The law, increasingly, has.

This article discusses general trends and Indian legal principles, and is not specific legal or financial advice. Speak to a family lawyer and a financial planner before acting on any of the above.

Found this useful? Share it.